Orderly Randomness

Quasirandom Numbers and Quasi–Monte Carlo

Brian Hayes

Harvard Institute for Applied Computational Science, 2015-02-06

Slides at: bit-player.org/extras/quasi

Part 1

Integration by Darts

Random Sampling

Darts:

Hits:

Area:

True area: 0.4178

Lattice Sampling

Darts:

Hits:

Area:

True area: 0.4178

Quasirandom Sampling

Darts:

Hits:

Area:

True area: 0.4178

Part 2

Varieties of Randomness

| • eurandom | (eu = good, true) |

| • pseudorandom | (pseudo = false, fake) |

| • quasirandom | (quasi = as if, seemingly) |

| • nonrandom | (non = not) |

Eurandom Numbers

- Unpredictable. (Also unrepeatable.)

- Uncorrelated, or independent.

- Unbiased, or uniformly distributed.

Eurandom Numbers

- Adversarial contexts: cryptography, gambling, proof.

- Need a source of entropy.

- A curious link between mathematics and physics, between the world of bits and the world of atoms.

Eurandom Numbers

- The gold standard, yet famously unreliable.

- Weldon and Tebb: after many years of rolling dice for science, Karl Pearson found an excess of fives and sixes.

- Almost always, the raw bits need to be “whitened.”

What could possibly go wrong?

A prime number for a cryptographic key, produced by the random number generator on a certain “smart card”:

10055855947456947824680518748654384595609524365

44429503329267108279132302255516023260140572362

51775707675238936398645381403154121089599274598

25236754563833

The same number written in binary:

11000000000000000000000000000000000000000000000

00000000000000000000000000000000000000000000000

00000000000000000000000000000000000000000000000

00000000000000000000000000000000000000000000000

00000000000000000000000000000000000000000000000

00000000000000000000000000000000000000000000000

00000000000000000000000000000000000000000000000

00000000000000000000000000000000000000000000000

00000000000000000000000000000000000000000000000

00000000000000000000000000000000000000000000000

000000000000000000000000000000001011111001

Pseudorandom Numbers

- Unpredictable. (Also unrepeatable.)

- Uncorrelated, or independent.

- Unbiased, or uniformly distributed.

Pseudorandom Numbers

Any one who considers arithmetical methods of producing random digits is, of course, in a state of sin.—von Neumann (1951)

Subtle is the Lord..., but he’s not out to get us.—Einstein (1921)

Pseudorandom Numbers

- Commonly generated by a linear recurrence, e.g.: \(x_k = a x_{k-1} + b \pmod{m}\).

- Not really uncorrelated: Finite cycle length, at most \(m\).

- Not really unbiased: Runs of 0s underrepresented.

Pseudorandomness: The Full Monte

\(x_k = 41 x_{k-1} + 1 \pmod{256},\quad x_0 = 3\)

Quasirandom Numbers

- Unpredictable. (Also unrepeatable.)

- Uncorrelated, or independent.

- Unbiased, or uniformly distributed.

Quasirandom Patterns

Quasirandom Numbers

- We’re in the realm of deterministic machines.

- They don’t pretend to be random.

- They don’t even look random.

What Is Randomness?

Philosophical musings

Part 3

A Slight Discrepancy

Counting points and measuring volume in axis-aligned rectangles

\[D(a,b) = \left\lvert\frac{\mathrm{count}[a,b)^2}{\mathrm{count}[0,1)^2} - \frac{\mathrm{vol}[a,b)^2}{\mathrm{vol}[0,1)^2}\right\rvert\]

Counting points and measuring volume in axis-aligned rectangles

\[D(a,b) = \left \lvert \mathrm{count}[a,b)^2 - \mathrm{count}[0,1)^2 \frac{\mathrm{vol}[a,b)^2}{\mathrm{vol}[0,1)^2}\right\rvert\]

Worst-case measure: \(\max\) over all axis-aligned rectangles \([a,b)^2\)

\[D = \max_{[a,b)^2 \in [0,1)^2} \left\lvert\frac{\mathrm{count}[a,b)^2}{\mathrm{count}[0,1)^2} - \frac{\mathrm{vol}[a,b)^2}{\mathrm{vol}[0,1)^2}\right\rvert\]

Star discrepancy: axis-aligned anchored rectangles

\[D* = \max_{[0,b)^2 \in [0,1)^2} \left\lvert\frac{\mathrm{count}[0,b)^2}{\mathrm{count}[0,1)^2} - \frac{\mathrm{vol}[0,b)^2}{\mathrm{vol}[0,1)^2}\right\rvert\]

Part 4

Quasi History

Mathematical Origins

- Ergodic theory: Well-stirred systems.

- Can we fill the unit interval uniformly?

- Simple arithmetic progression seems to be the answer.

- But how do we add points one at a time while preserving uniformity?

Covering the Interval [0, 1)

- Hermann Weyl 100 years ago: the sequence \(\alpha, 2\alpha, 3\alpha,\dots,n\alpha \pmod{1}\) is equidistributed if \(\alpha\) is any irrational number.

- Proved by an argument about Riemann integrals that leads directly to the idea of Monte Carlo integration.

- Irrationality is necessary; without it, only a finite set of fractions.

- Irrationality is inconvenient for finite computing machines.

Covering the Interval [0, 1)

- Johannes van der Corput, 1930s: Asked if any sequence could have discrepancy bounded by a constant for all N.

- In other words, if the discrepancy is given by some function \(f(N)/N\), can \(f(N)\) remain below some constant \(C\) as \(N\) goes to infinity?

- The answer is no. Proved in the 1940s by Tatyana Pavlovna van Aardenne-Ehrenfest.

- Stronger bounds by K. F. Roth in the 1950s, and others.

- Extensions to point sets in two or more dimensions.

A First Attempt

at Quasi-MC

- R. D. Richtmyer, Los Alamos, 1951.

- Problem of neutron diffusion (same as first MC studies).

- A Weyl sequence: \(n \alpha \pmod 1 \) for irrational \(\alpha\).

- Outcome: No better than ordinary Monte Carlo.

- But he published the negative result! (This is to be encouraged: You can claim priority even for your failures.)

Part 5

Making Quasirandom Numbers

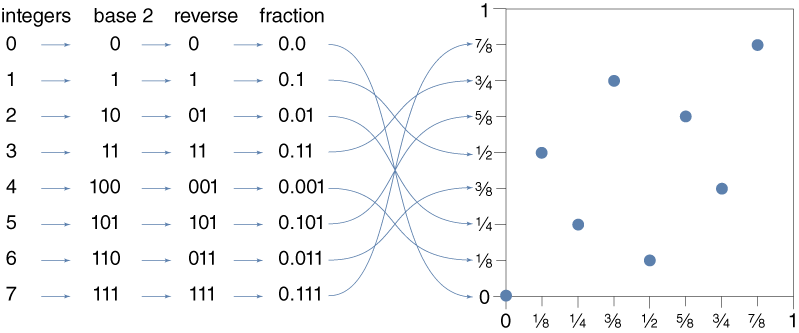

Van der Corput Procedure

Quasirandomness Generators

- Van der Corput algorithm is a bizarre mashup of operations on numbers and operation on numerals—the representation of numbers.

- Other quasirandom generators are just as strange.

- Maybe this sort of bit-twiddling is where the “randomness” comes from in quasirandom sequences.

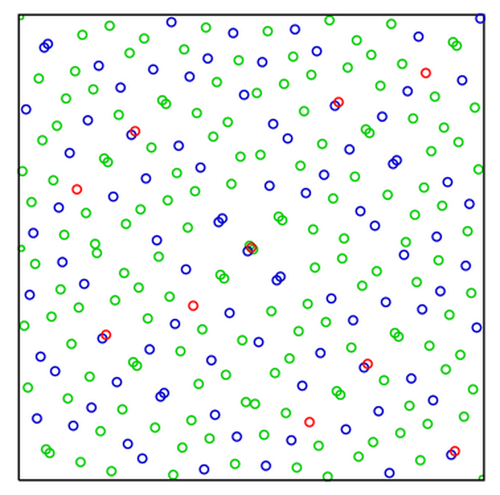

I. M. Sobol Quasipattern

Part 6

Convergence Rates

Convergence Rates

- How many points do you have to sample to achieve a given accuracy?

- For pseudorandom Monte Carlo, the expected sampling error is proportional to \(\sqrt{N}/N\).

- This bound follows from the law of large numbers or the central limit theorem.

Convergence Rates

- In quasi-Monte Carlo, the corresponding expected error goes as \((\log N)^{d}/N\), where \(d\) is the spatial dimension.

- Trading \(\log N\) for \(\sqrt{N}\) is potentially a huge improvement: the square root of 1,000,000 is 1,000, but \(\log_{2}\) 1,000,000 is only 20.

- But there’s that pesky exponent \(d\). For any fixed \(d\), \(\sqrt{N}/N\) will eventually exceed \((\log N)^{d}/N\), but it may take a very large value of \(N\) to reach the crossover.

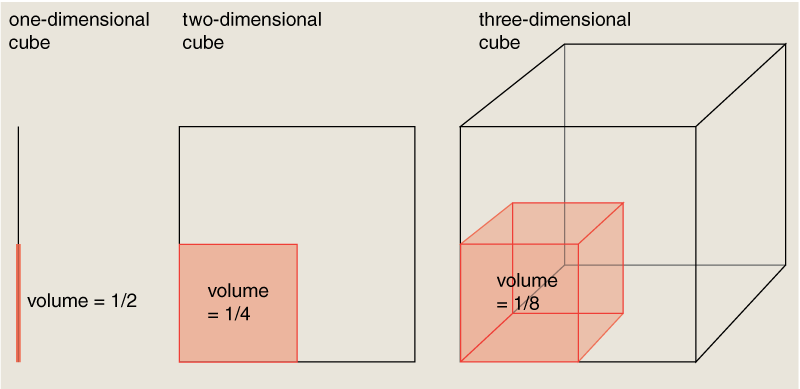

The Curse of Dimensionality

- In high dimensions, all the volume is in the corners.

- Measuring that volume, effort grows as \(2^d\).

Another Problem: Error Estimates

- Randomness in conventional MC yields an intrinsic error estimate: Just measure the variance of multiple trials.

- Deterministic methods (quasi or lattice) have no concept of variance.

The Twilight of Quasi-MC

The situation from the 1950s into the 1990s:

- Quasi-Monte Carlo has a theoretical advantage in low dimensions.

- But most low-dimensional problems are easy for any numeric integration scheme.

- For pseudorandom MC, the \(\sqrt{N}\) convergence rate is less than wonderful, but it does have the virtue of being independent of dimension.

- As a result, quasi-MC was largely set aside by practitioners, although mathematical work continued.

Part 7

A New Dawn for Quasi-MC

Financial Engineering

- Collateralized mortgage obligation (CMO): One of the clever inventions that brought us the great recession of 2008.

- Gathers thousands of mortgage loans into a single, marketable security.

- Whether you’re buying or selling, you need a way to assign a price to a specific CMO.

Pricing a CMO

- Isn’t this a straightforward problem of calculating net present value?

- A 30-year mortgage represents a stream of 360 monthly payments; you apply a discount rate to determine how much you ought to pay now for the promise of a dollar 30 years hence.

- But most mortgages do not survive for a full 360 monthly payments. When a house is sold or refinanced, the balance is paid in advance. There’s also the possibility of default.

Monte Carlo on Wall Street

- Formulate the problem as an integral in a space of 360 dimensions.

- For evaluating such integrals Monte Carlo methods are favored not because they work well but because nothing else works at all.

- The use of such techniques, borrowed from physics or computer science, became part of the great “quant” revolution in finance in subsequent years.

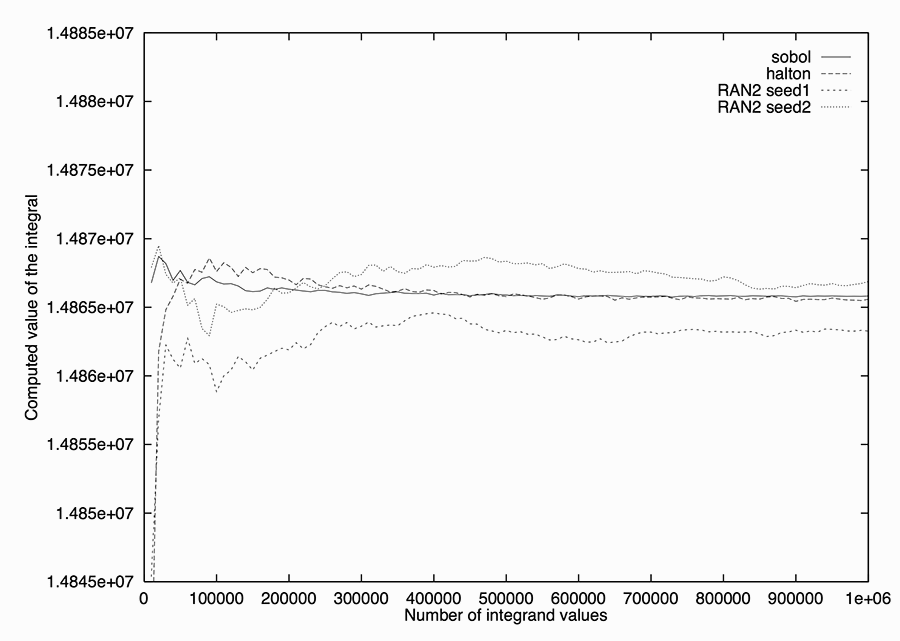

Quasi-Monte Carlo on Wall Street

- In 1992 Goldman Sachs, the investment bank, approached Joseph Traub’s group at Columbia seeking advice on methods for evaluating CMOs.

- Traub and several graduate students, including Spassimir Paskov, decided to try quasi-Monte Carlo, ignoring the received wisdom.

- It worked. Convergence was faster by a factor between 2 and 5.

The Aftermath

- Paskov earned his degree and went to work for a Swiss bank.

- Traub, Paskov, and another colleague received a patent related to the work.

- Use of quasi-MC spread rapidly through the world of investment banking.

- Twelve years later, the economy tanked. (Causation?)

- Meanwhile, the small community of quasi-fanatics went to work figuring out what it all means.

Part 8

Quasi Miracles?

Laws of Nature Still Enforced

- The earlier results on convergence rates and accuracy were not wrong.

- The curse of dimensionality has not been lifted.

- Fully evaluating a 360-dimensional integral requires \(\approx 2^{360}\) samples, not \(10^{6}\).

- \(\therefore\) either the quasi-MC technique is more powerful than we knew, or the problem is easier than it looks.

Effective Dimensions?

- The Paskov-Traub result provoked a spate of quasi reassessments (e.g., [Caflisch 1998], [Owen 2002], [Sloan 2005].

- The verdict: The 360-dimensional integral doesn’t really have 360 “effective” dimensions.

- ANOVA approach: If almost all the variance lies in a few dimensions, the rest can be truncated.

- Analogous to compressed-sensing.

Open Questions

- How do we recognize that a problem has effective dimensionality lower than its formal dimensionality?

- How common are such problems?

- Will quasirandom methods work for other kinds of Monte Carlo studies (e.g., random walks, percolation, statistical mechanics, optimization)?

Thanks!

Bibliography (PDF)

brian@bit-player.org

Start Over